Islamic Fintech is still in its early phase; nonetheless, its potential disruptions to traditional Islamic banking and finance (IBF) should not be underestimated.

According to the assistant governor of Malaysia, Mr Marzunisham Omar, “The growth of Fintech provides “innovative opportunities” within the entire financial sector and thus Islamic Fintech cannot be ignored by the IBF industry, particularly in Malaysia”. Fintech has been growing speedily with a global investment reported to be at USD19 billion in 2015, compared to only USD1.8 billion in 2010.

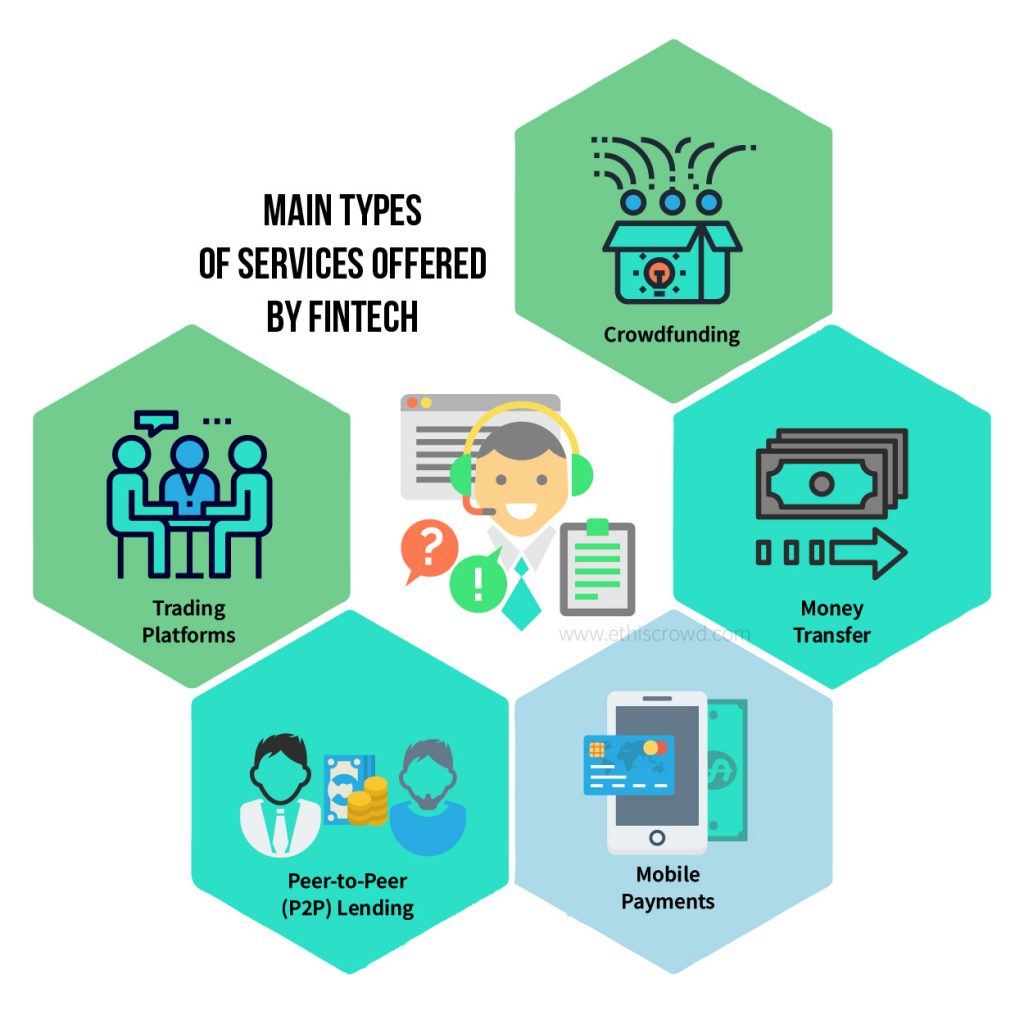

The main types of services offered by Fintech are peer-to-peer (P2P) lending, crowdfunding, money transfer, mobile payments and trading platforms. In addition, there are also Fintech services for other sub-segments such as wealth management, insurance, etc.

In the Islamic finance arena, there are a few prominent Islamic Fintech companies among others include Singapore-based KapitalBoost, Malaysia-based Ethis Kapital Sdn. Bhd. which operates NusaKapital.com and US-based Wahed Invest LLC in the segments of P2P lending and crowdfunding.

Opportunities

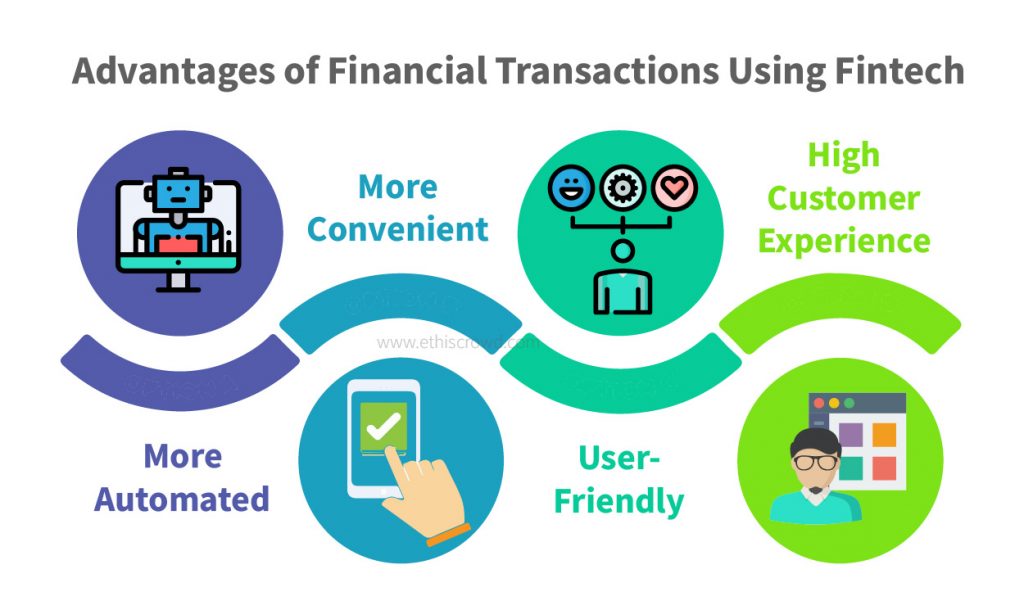

Fintech creates various opportunities. For instance, through Fintech, financial transactions will become more automated, user-friendly and more convenient, leading to a higher customer experience.

According to IFSB secretary-general Jaseem Ahmad, “There are tremendous opportunities for Islamic Fintech and Islamic banking institutions (IBIs) are taking up Fintech to reach out and improve the attractiveness of their products at a lower cost”. Also, the IBF industry currently reaches approximately 100 million customers worldwide, however, the potential market is six times that, and this gap can also be tapped through Fintech.

In addition as reported by the World Bank, with the presence of Fintech, approximately two billion adults who are currently unbanked will now have access to financial solutions. Moving to the Southeast Asian (SEA) region, only 27% of the region’s 600 million people have a bank account and approximately 40% of the unbanked are Muslims. This serves as an impetus for Islamic Fintech in addressing financial inclusion. With the availability of Shariah-compliant crowdfunding and P2P financing tools, this creates opportunities for individuals and SMEs who require financing but thus far do not qualify for financing from traditional IBIs. For example in the case of Singapore-based Islamic Fintech company KapitalBoost, it offers SMEs, who are often disadvantaged in their access to funds for business expansion, short-term financing alternatives with fast and friendly approval process and at competitive rates. Financing is provided through Shariah-compliant structures such as Murabaha, Qard, Wakalah etc.

Overall with Fintech services, it can help the unbanked to create a new form of credit history and moving from there, at the next phase they can then be served by the larger IBF.

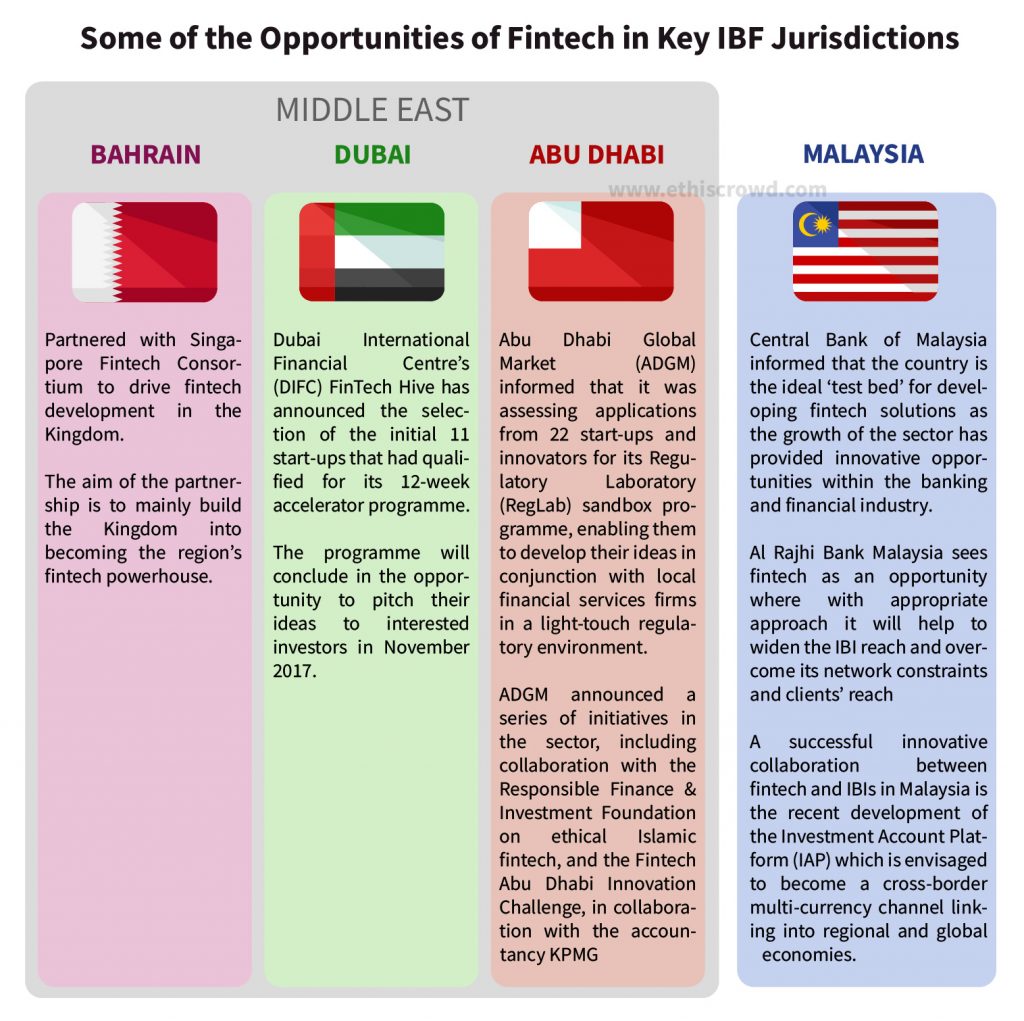

Opportunities of Fintech in Key IBF Jurisdictions

In the Middle East region, key IBF jurisdictions such as Bahrain, Dubai and Abu Dhabi sees Islamic Fintech as a huge opportunity. Bahrain has recently partnered with the Singapore Fintech Consortium to drive Fintech development in the Kingdom. The aim of the partnership is to mainly build the Kingdom into becoming the region’s Fintech powerhouse. Moving to Dubai, the Dubai International Financial Centre’s (DIFC) FinTech Hive has recently announced the selection of the initial 11 start-ups that had qualified for its 12-week accelerator programme, which will conclude in the opportunity to pitch their ideas to interested investors in November 2017. On the other hand, Abu Dhabi Global Market (ADGM) recently informed that it was assessing applications from 22 start-ups and innovators for its Regulatory Laboratory (RegLab) sandbox programme, enabling them to develop their ideas in conjunction with local financial services firms in a light-touch regulatory environment. ADGM, which positioned itself as a Fintech hub from when it first opened its doors in 2016, has announced a series of initiatives in the sector, including collaboration with the Responsible Finance & Investment Foundation on ethical Islamic Fintech, and the Fintech Abu Dhabi Innovation Challenge, in collaboration with the accountancy KPMG.

Other key IBF jurisdiction such as Malaysia also sees Islamic Fintech as an opportunity. According to Al Rajhi Bank Malaysia, Islamic Fintech is seen as an opportunity where with appropriate approach it will help to widen the IBI reach and overcome its network constraints and clients’ reach. Furthermore, Central Bank of Malaysia has also said that the country is the ideal ‘test bed’ for developing Fintech solutions as the growth of the sector has provided innovative opportunities within the banking and financial industry. A successful innovative collaboration between Fintech and IBIs in Malaysia is the recent development of the Investment Account Platform (IAP) which is envisaged to become a cross-border multi-currency channel linking into regional and global economies. Parallel to other Fintech platforms such as crowdfunding and peer-to-peer lending, IAP facilitates direct investment by investors in viable ventures of their choices, nonetheless, a key differentiating factor of IAP is the roles undertaken by IBIs – it will provide investors with direct access to a broad range of investment opportunities, and businesses as well as IBIs with a new source of funding.

Threats

On the flip side, even though Islamic Fintech can be seen as an opportunity for the ‘unbanked’ segment of the society, the same opportunity can be seen as a threat to the IBIs. For instance, with the establishment of Islamic Fintech companies, it can potentially lead to the SMEs increasingly favouring services offered by these companies as it proposes simple, low-cost alternative financing instead of tedious and lengthy procedures offered by IBIs. These Islamic Fintech companies focus on connecting creditworthy business looking for funding with smart investors to build mutually beneficial partnerships of growth, by applying the innovative technology of crowdfunding to eliminate the costs and complexity associated historically with banks. The consultancy and auditing firm EY (formerly Ernst & Young) in its 2016 Global Consumer Banking survey informed that four out of 10 customers reported reduced dependence on their bank as their primary financial services provider, and increasingly relying on Fintech providers instead. In addition, a survey of large financial institutions conducted earlier this year by PwC (PricewaterhouseCoopers) found that approximately 90 percent feared their business was at risk from emerging Fintech players, possibly resulting in established players losing up to 24% of their revenues in the next three to five years. Furthermore, Citi projected last year that Fintech startups will prompt banks in the US and Europe to remove 1.7 million jobs, or more than 305 of their total workforce, by 2025.

To avoid having Fintech as an existential threat to IBIs, it is essential for IBIs to move more rapidly to embrace digital strategies and developments to avoid the risk of losing market share to Fintech players, which are gradually making inroads into the financial landscape. Furthermore, Fintech players have the ability to innovate at speeds difficult for IBIs to match, thus it is important for IBIs to disrupt itself before someone else does it for them. RHB Bank Bhd. COO Rohan Krishnalingam shared similar sentiment by stating that Fintech is both a threat and an opportunity to traditional banks. He further highlighted that “If banks don’t change, it’s a threat; although it’s also an opportunity to adapt to technologies, to be more efficient and bring new innovations to the market. So Fintech is already a focus for us and will continue to going forward – if we don’t do it, somebody else will”.

Concluding Remarks

Moving forward, to fully utilize the functionality that new Fintech can offer, IBIs must quickly address the cumbersome technological constraints to effectively adopt the technology. Whether it is a digital solution or blockchain technology, IBIs must ensure their back office is truly real-time and adaptable. Also, instead of seeing Fintech firms as a threat or competition, IBIs should find ways to collaborate with Fintech companies in order to stay competitive.

Through appropriate collaborations, IBIs can learn from the innovative practices of the newly emerged Islamic Fintech start-ups and consequently, the Islamic Fintech start-ups can learn the ins and outs of doing business with established IBIs. With proper and effective collaborations, and after taking into considerations all of the threats and opportunities that must be in accordance to Shariah, together they can benefit from the growth multiplier that Fintech can offers.

Read more on the Sustainable Development of an Islamic Financial System

One Reply to “Islamic Fintech – A Threat for Islamic Banks or an Opportunity?”

If you guys are looking for the list of islamic fintech startups or want to submit your own startup. Do it here > https://forum.islamicfintech.org//t/here-is-the-list-of-more-than-100-islamic-fintech-startups/96

Top Posts

Islamic P2P Crowdfunding Explained

How to Earn Halal Money? The Money Mindset

Halal Investments for Singapore Muslims? It’s time for a shake-up in the Islamic Investments scene.

Smart investment for making Halal money

3 Reasons Why Property Crowdfunding is the Smart Investment for You